…and that is why most people find themselves staring at a screen at midnight, trying to make sense of why the numbers keep moving. If you are looking for a straight answer on how to secure a home in the Grand Canyon State right now, it comes down to one reality: the market is no longer a monolith of low rates and easy credit.

Securing a mortgage in Arizona today requires a specific strategy tailored to your local geography and your specific credit profile. Whether you are looking at a bungalow in Mesa or a sprawling lot in Scottsdale, the math changes depending on whether you are eyeing a standard 30-year fixed or a specialized product like an FHA loan.

The direct answer to the question of what you should do is this: stop chasing the absolute lowest interest rate and start looking at the total cost of your loan over its lifetime. A slightly higher rate with a lower closing cost might actually save you thousands if you plan to move in five years, whereas a low rate with heavy points might be a trap.

Arizona buyers are currently navigating a split reality. On one hand, inventory in the Phoenix metro area remains tight, which keeps price competition high. On the other hand, the availability of various loan products means there is a way through the door for almost everyone, provided they know which door to knock on.

You need to understand that your local lender’s “sticker price” isn’t your final number. Between private mortgage insurance (PMI), escrow accounts for property taxes, and the rising cost of homeowners insurance in some desert regions, the monthly payment is often higher than the interest rate alone suggests.

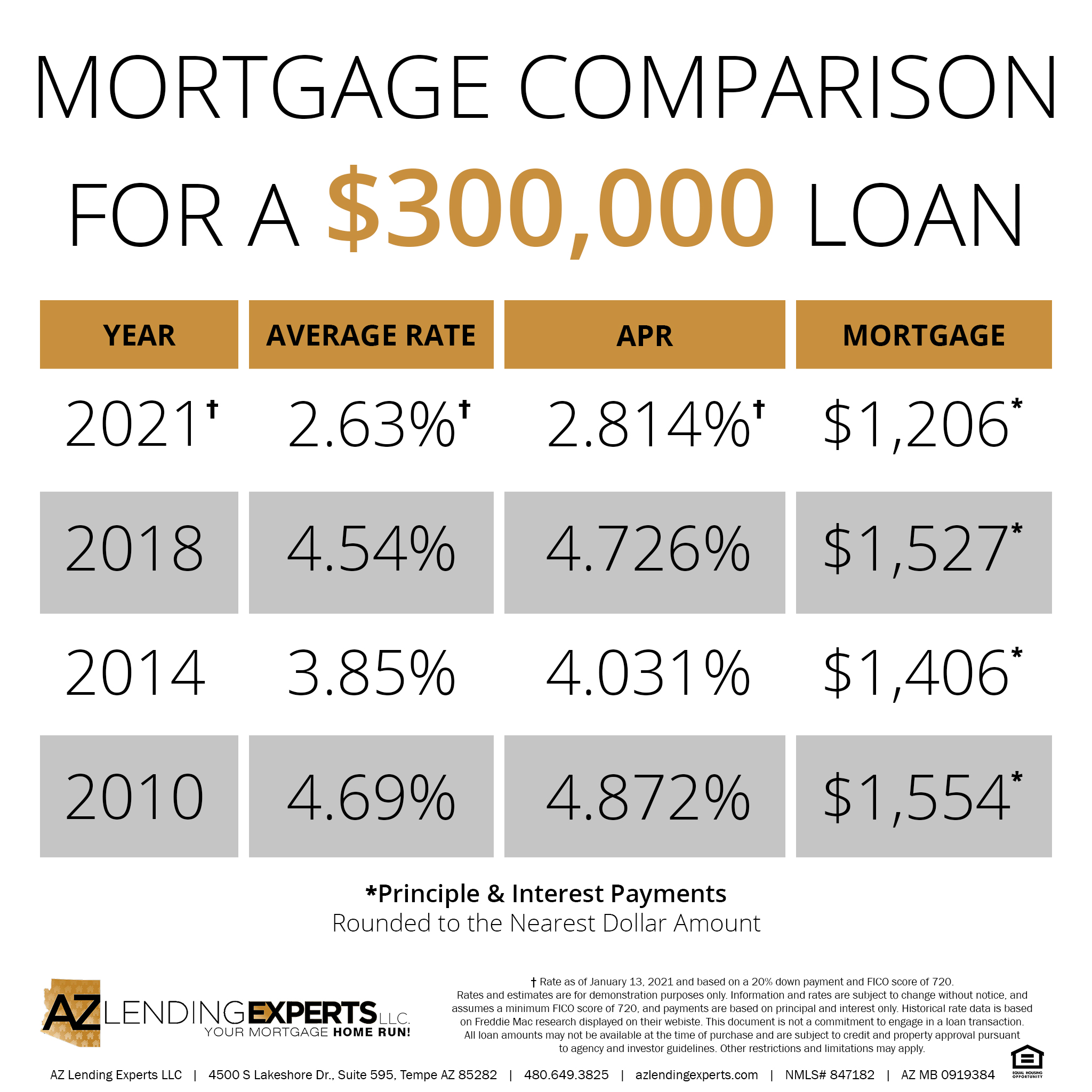

The Reality of Current Rate Fluctuations

Rates don’t move in a straight line, and they certainly don’t care about your personal timeline. Most people think they can time the market, waiting for that perfect dip that never quite arrives. In reality, the market reacts to Federal Reserve signals and inflation data, often before you even finish reading the morning news.

If you look at the data provided by U.S. Bank, you will see that rates change daily. This volatility is a double-edged sword. It means you might find a better deal tomorrow, but it also means the house you love might become $300 more expensive per month by next Tuesday.

Many buyers get stuck in “analysis paralysis.” They spend six months watching the ticker symbols on finance apps, only to realize that home prices in their preferred suburb rose by 5% during that same period. The cost of waiting often outweighs the savings from a fractional decrease in interest rates.

It helps to categorize your options. You aren’t just choosing between 15-year and 30-year terms. You are choosing between stability and flexibility. Some people prefer the certainty of a fixed-rate mortgage, while others might look at adjustable-rate options if they know they will only hold the home for a short period (though this is a gamble).

When you sit down with a lender, ask about the “spread.” This is the difference between what it costs the bank to borrow money and what they charge you. If you see a massive gap, you might be looking at a lender with high overhead or one that is padding their margins significantly.

Decoding Loan Types for Arizona Buyers

Not all loans are created equal, and the “best” loan is entirely dependent on your down payment capacity and your credit score. A buyer with a 740 score has a completely different toolkit than a first-time buyer with a 620 score. This is where the nuance of the Arizona market becomes visible.

FHA loans remain a staple for those who might not have a massive pile of cash for a down payment. These loans are more forgiving of lower credit scores, but they come with the requirement of mortgage insurance, which can add a significant chunk to your monthly bill. It is a trade-off between getting into a home now versus paying more for the privilege of a lower entry barrier.

Jumbo loans are another beast entirely. If you are shopping in high-end markets like Paradise Valley, your loan amount will likely exceed the conforming loan limits. These loans often require higher credit scores and more substantial cash reserves. You can’t just walk in with a standard application; the underwriting is much more stringent.

For those who are veterans or active-duty service members, VA loans are a massive advantage. They often require zero down payment and have very competitive rates. It is one of the few programs that actively works in your favor rather than just being a “standard” option. If you qualify, you should take it seriously.

| Loan Type | Best For… | Primary Down Payment Requirement |

|---|---|---|

| Conventional | Buyers with high credit scores | Typically 3% to 20% |

| FHA | First-time buyers or lower credit | 1.65% to 3.5% |

| VA | Veterans and Service Members | 0% |

| Jumbo | Luxury homes/High loan amounts | Often 10% to 20% |

Understanding these distinctions early in the process prevents a lot of heartbreak. There is nothing worse than finding your dream home in Gilbert, getting your heart set on it, and then finding out your credit score won’t allow for the specific loan you needed to make the numbers work. I remember a client, let’s call him Dave, who spent three months looking at houses only to realize his self-employed income was being calculated differently by a conventional lender than he had expected. He ended up needing an FHA loan to bridge the gap, which changed his entire budget.

If you want to explore your specific options, checking current Arizona mortgage rates can give you a baseline for what the market is doing at this exact moment. It isn’t a guarantee, but it is a starting point for your math.

The Local Lender Advantage vs. Big Banks

You have a choice between the giant national banks, the online lenders, and the local Arizona-based institutions. Each has a distinct personality and a different set of pros and cons. The national lenders are often the fastest and have the slickest apps, but they can feel like a black hole once you submit your paperwork.

Local lenders, like those offered by the National Bank of Arizona, often have a deeper understanding of the local property values and the specific nuances of Arizona real estate. They might be more willing to look at a situation that a computer in a different time zone would automatically reject. There is a “human” element that matters when a deal is on the line.

Online lenders are incredibly convenient if you want to do everything from your couch. They are often very competitive on price because their overhead is lower. However, if something goes wrong with your closing, and in real estate, something almost always goes wrong, getting a human on the phone can feel like trying to catch smoke with your hands.

When you are vetting lenders, don’t just look at the rate. Look at the “Loan Estimate” document. This is a standardized form that every lender is legally required to give you. It’s the only way to truly compare “apples to apples.” If one lender shows a low rate but has a high “origination fee,” they are essentially charging you the interest upfront.

Using resources like top-rated mortgage lenders in Arizona can help you see how others in the community view these companies. Peer reviews and investment specialties matter because a lender that specializes in rental properties will handle a fix-and-flip loan very differently than one that specializes in primary residences.

Hidden Costs and the Total Cost of Ownership

Your mortgage payment is not just principal and interest. This is the biggest mistake new homeowners make. When you see a listing for a $2,500 monthly payment, you have to account for the “PITI” (Principal, Interest, Taxes, and Insurance). In Arizona, property taxes are generally manageable, but insurance is a different story.

Homeowners insurance costs vary wildly depending on where you are located. A house near a wildfire-prone area or in a region with high storm activity will command much higher premiums. You should call your insurance agent before you even get pre-approved so you aren’t shocked by the monthly escrow requirement.

Then there is the “hidden” maintenance. A house in the desert deals with specific issues, AC units working overtime in July, dust, and potential monsoon damage. You need to build a “house fund” that exists entirely separate from your mortgage payment. If you are spending every extra cent on your mortgage, you are one broken water heater away from a crisis.

Don’t forget about the closing costs. These typically run anywhere from 2% to 5% of the home’s purchase price. Many people forget to save for this, assuming it will be rolled into the loan. While you can sometimes do that, it increases your total debt and can change your interest rate tier. It’s better to have that cash sitting in a high-yield savings account ready to go.

The math is always going to be more complex than a simple calculator makes it seem. The goal is to find a rhythm where you aren’t just surviving the month, but actually building equity. If your mortgage is too heavy, you’re just a tenant for the bank. Aim for a lifestyle where the house is an asset, not a weight.

The market will keep shifting, and the rates will continue to dance. The best thing you can do is prepare your finances today so you can act when the right opportunity appears. For the full picture, it’s worth checking arizonaziploan.com.

Good to know

What are the different types of mortgage loans available in Arizona?

Common options include conventional loans, FHA loans for lower down payments, VA loans for veterans, and USDA loans for qualifying rural properties.

What is the typical credit score required for an Arizona mortgage?

While requirements vary by loan type, conventional loans usually require a score of 620 or higher, while FHA loans can go as low as 580.

How much can I borrow for a home in Arizona?

Your borrowing capacity depends on your debt-to-income ratio, credit score, and down payment, as well as specific county-level loan limits set by Fannie Mae and Freddie Mac.

Do I need a large down payment for a mortgage in Arizona?

Not necessarily; while 20% is standard to avoid private mortgage insurance, FHA loans allow as little as 3.5% down and some programs offer 0% down options.

How long does the mortgage approval process take in Arizona?

The process typically takes between 30 to 45 days from the time the application is submitted to the closing date.